Market Pulse

U.S. crude inventories fell by 12.4 million barrels last week, including a 3.3 million barrel draw from commercial stocks and an 11.1 million barrel release from the SPR. Gasoline inventories declined by 2.6 million barrels and diesel inventories fell by 2.1 million barrels, both driven by strong demand. Propane stocks also decreased by 0.4 million barrels, while exports surged to 2.625 million barrels per day, well above the four-week average of 2.206 million barrels per day. Additional export capacity is expected soon following Enterprise’s Houston Ship Channel terminal expansion.

According to the EIA, commercial crude inventories now stand at 441.7 million barrels, roughly 2% below the five-year average. The API had previously reported a 2.8 million barrel crude draw for the same period.

Crude prices rebounded Thursday, with Brent rising to $96.74 per barrel and WTI climbing to $91.12, though both remain significantly below last week’s levels. Meanwhile, total U.S. petroleum demand averaged 20.2 million barrels per day over the past four weeks, up 1.5% year over year.

Fundamentals

EIA’s Weekly Petroleum Inventory in MM’s BBLS

| Commodity | US Inventory | Change | 5 Yr Ave | CURRENT MARKETS |

|---|---|---|---|---|

| Crude Oil | 441.7 | -3.3 | 454 | WTI Crude: 0.34 |

| Gasoline | 211.6 | -1.5 | 227 | Heating Oil: 0.0130 |

| Distallates | 100.8 | 0.4 | 114 | RBOB: 0.0289 |

| Commodity | US Inventory | Change | Midwest Invent | Change |

|---|---|---|---|---|

| Propane | 81.2 | -0.4 | 17.7 | 0.4 |

Propane

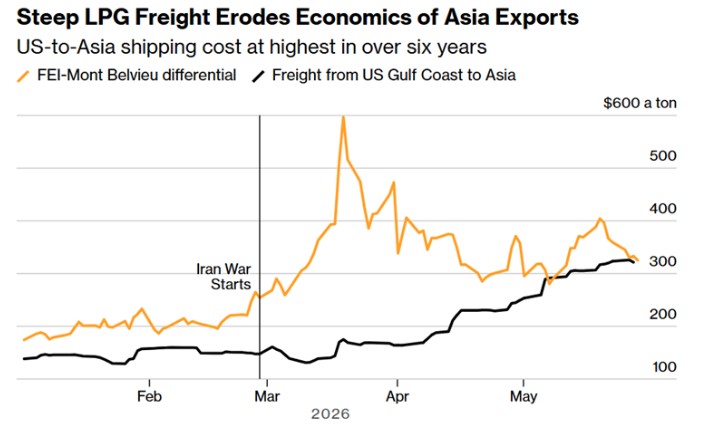

Despite weakening U.S.-to-Far East export economics driven by surging ocean freight rates, primary propane hubs strengthened relative to broader energy markets, with Conway rising 2% and Mt. Belvieu gaining 1.4% versus WTI crude. Increased wholesaler buying activity across both hubs provided support, as some market participants viewed the recent price pullback as a buying opportunity.

In export markets, two June-loading Gulf Coast cargoes were reportedly canceled amid sharply higher freight costs, ongoing Panama Canal congestion, elevated transit fees, and softer international demand, all of which have narrowed export arbitrage opportunities.

Consequences of the SPR drawdown

The continued drawdown of the Strategic Petroleum Reserve is influencing both U.S. crude inventories and global oil markets, as a significant portion of released barrels continues flowing overseas.

While SPR releases help increase near-term supply availability and moderate domestic inventory draws, many of those barrels are being exported to Europe and Asia, where refiners have relied heavily on U.S. crude following disruptions to Russian supply. European refining hubs in particular have become increasingly dependent on U.S. exports to stabilize regional energy markets.

If the U.S. were to halt exports of SPR-related crude, domestic inventories would likely rise sharply, placing downward pressure on WTI prices and widening the spread to Brent crude. While U.S. refiners could benefit from lower feedstock costs, oversupply conditions could eventually pressure shale production growth.

Globally, Europe would likely face tighter crude supplies, higher feedstock costs, and increased competition for alternative barrels from the Middle East and West Africa. Reduced U.S. exports could also contribute to higher diesel and transportation fuel prices across the region.

For now, SPR releases continue providing short-term supply relief to both domestic and international markets, though the eventual end of those drawdowns could tighten global balances if production growth fails to offset the loss of government barrels.

Humor

Disclaimer: The data, information and related graphics (collectively, “Information”) is for general information use only and is compiled from sources believed to be reliable. Dale Petroleum Company does not guarantee its accuracy or completeness, nor does DPC assume any liability for any inaccurate or incomplete information. The Information is not intended to be a research report nor an analysis of a company and it should not be relied upon for making investment decisions. The information is subject to change without notice, is for general information only and is not intended as any offer or solicitation with respect to the purchase or sale of any financial instrument or as personal investment advice.