Market Pulse

U.S. crude oil inventories fell by 7.9 million barrels for the week ending May 15, according to the U.S. Energy Information Administration (EIA), bringing total stockpiles to 445.0 million barrels, about 2% below the five-year seasonal average. The decline followed a 9.1 million-barrel draw reported by the American Petroleum Institute.

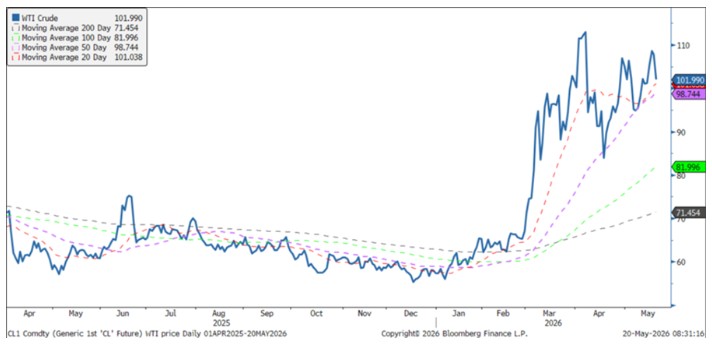

Oil prices moved lower on Wednesday, with Brent crude at $108.90 per barrel (-2.17%) and West Texas Intermediate (WTI) at $102 (-2.05%) amid market reactions to geopolitical comments from U.S. President Donald Trump.

Gasoline inventories decreased by 1.5 million barrels after a 4.1 million-barrel draw the previous week, while distillate stocks rose by 400,000 barrels. Distillate inventories remain 9% below the five-year average. Gasoline production averaged 9.3 million barrels per day, while distillate production averaged 5.0 million barrels per day.

Total petroleum products supplied, a proxy for demand, rose to 20.2 million barrels per day over the past four weeks, up 3.1% year over year. Gasoline demand averaged 8.9 million barrels per day, and distillate demand averaged 3.6 million barrels per day, up 1.4% year over year.

Fundamentals

EIA’s Weekly Petroleum Inventory in MM’s BBLS

| Commodity | US Inventory | Change | 5 Yr Ave | CURRENT MARKETS |

|---|---|---|---|---|

| Crude Oil | 445.0 | -7.9 | 454 | WTI Crude: -4.85 |

| Gasoline | 214.2 | -1.5 | 227 | Heating Oil: -0.1915 |

| Distallates | 102.9 | 0.4 | 114 | RBOB: -0.1655 |

| Commodity | US Inventory | Change | Midwest Invent | Change |

|---|---|---|---|---|

| Propane | 81.6 | 0.4 | 17.7 | 0.4 |

Propane

Propane hub pricing was largely unchanged Tuesday, as market conditions continue to reflect the same underlying narrative seen in recent weeks. Propane prices remain closely tied to movements in crude oil, particularly as uncertainty surrounding the closure of the Strait of Hormuz persists. Prices are expected to remain elevated until a definitive resolution is reached.

In the near term, some modest price relief could emerge following today’s EIA inventory report. According to the average estimate from an OPIS survey conducted Tuesday, the Energy Information Administration is expected to report a 1.8 million-barrel build in U.S. propane/propylene inventories in Wednesday’s Weekly Petroleum Status Report.

Backwardation Signals Rising Oil Supply Fears

Backwardation occurs when near-term oil contracts trade at higher prices than contracts for future delivery, signaling that the market values immediate oil supply more highly than future supply. For example, if July crude trades at $82 per barrel while December crude trades at $76, traders are paying a premium for oil available today.

This structure typically reflects strong current demand, tight short-term supply, and concerns about disruptions such as geopolitical conflict or refinery outages. It also discourages storage because companies lose money holding barrels that can be sold at higher prices immediately.

The current oil market is in backwardation largely due to tensions involving Iran and risks surrounding the Strait of Hormuz, a critical global oil shipping route. Traders fear disruptions to tanker traffic, reduced Gulf exports, and rising shipping and insurance costs. As a result, prompt barrels have become especially valuable.

At the same time, lower prices further out on the futures curve suggest the market believes these disruptions may eventually ease through diplomacy, increased OPEC+ production, rerouted exports, or weaker demand. In this sense, the oil curve is acting as a geopolitical stress gauge, reflecting immediate fear more than a permanent supply shortage.

Backwardation can also create longer-term bullish conditions. Because it discourages storage, inventories tend to decline, leaving the market more vulnerable to future supply shocks. Ongoing geopolitical instability may also reduce investment in production and infrastructure, while strong prompt demand signals resilient global consumption.

However, the bullish structure could reverse quickly if tensions de-escalate, tanker traffic normalizes, OPEC+ boosts production, or economic growth slows. For now, backwardation remains a clear sign that the market is focused on immediate supply risk and elevated geopolitical uncertainty.

Funny

Disclaimer: The data, information and related graphics (collectively, “Information”) is for general information use only and is compiled from sources believed to be reliable. Dale Petroleum Company does not guarantee its accuracy or completeness, nor does DPC assume any liability for any inaccurate or incomplete information. The Information is not intended to be a research report nor an analysis of a company and it should not be relied upon for making investment decisions. The information is subject to change without notice, is for general information only and is not intended as any offer or solicitation with respect to the purchase or sale of any financial instrument or as personal investment advice.